IASB's Exposure Draft and its impact for financial institutions

The International Accounting Standards Board (IASB) has extended the comment period for its Exposure Draft Risk Mitigation Accounting until 30 November 2026. It proposes amendments to IFRS 9 Financial Instruments and IFRS 7 Financial Instruments: Disclosures, and details a new model for Risk Mitigation Accounting (RMA) in response to feedback that current hedge accounting does not fully reflect how institutions manage interest rate risk.

The goal is to create a model that accurately reflects a company's risk management activities in its financial statements, thereby enhancing transparency for all stakeholders. These proposed changes affect both IFRS 9 and IFRS 7 and will be significant for banks globally.

Hedge accounting has always aimed to align the accounting view of the world with the economic one. The RMA proposal is the next step in this evolution, moving toward dynamic risk management. The IASB is proposing:

Scope of risk mitigation accounting, IASB’s Exposure Draft Snapshot

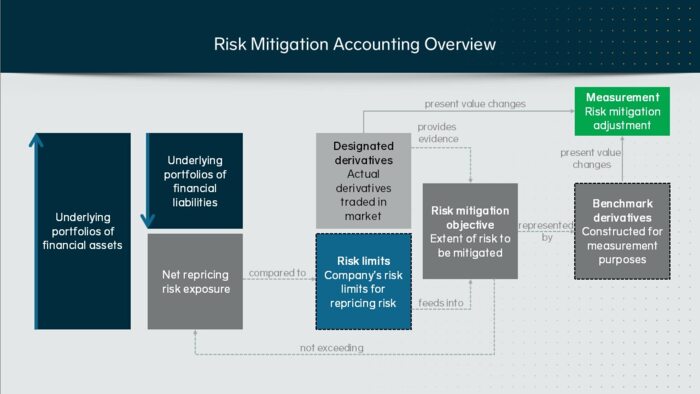

A crucial, unstated goal of the RMA proposal is to create a direct bridge between the accounting operations, treasury, and the Asset-Liability Management (ALM) function. While hedge accounting has traditionally been the domain of the treasury department, the strategic, portfolio-wide nature of RMA elevates the role of ALM. The RMA model essentially adopts the ALM playbook. Concepts like Net Repricing Risk Exposure, and the use of time bands are standard practice for any ALM desk. By formalizing this approach, RMA ensures that the economic results of the ALM team's risk management activities are more faithfully represented in the financial statements.

For this to succeed, these three functions will require tighter integration than ever before. The strategic decisions from the ALM team and the execution from treasury will now become direct input to financial reporting, requiring a new level of collaboration and shared data.

The IASB has extended the comment period for the Exposure Draft to 30 November 2026. This decision was made to give stakeholders more time to consider the technical and operational aspects of the proposals and to allow companies undertaking fieldwork to use those results to inform their comments. This extension makes it a critical time for banks to analyze the strategic implications.

We recommend the following preparatory steps:

The proposed modernization of hedge accounting represents a significant regulatory shift. While the compliance challenge is substantial, it also presents an opportunity to gain a strategic advantage.

Partnering with Regnology allows you to leverage a proven, standardized solution. Our deep domain expertise in regulatory reporting and risk management is embedded in our Regnology Finance Hub, ensuring you can navigate this transition with efficiency and confidence. We provide the structure and control needed to manage dynamic risk positions, freeing your team to focus on business requirements.

© 2026 Regnology Group GmbH All Rights Reserved

DE

DE  FR

FR